+91 7014607737

+91 7014607737

info@technoloader.com

info@technoloader.com

Table of Contents

Blockchain compliance now decides which projects scale. Without it, you get shut out of banking, payments, and serious customers.

I have seen this across the 450+ projects we have delivered at Technoloader. The platforms that last built compliance in from the first sprint. They do not bolt it on later.

The stakes climbed sharply in 2025. The United States passed its first federal crypto law, the GENIUS Act. Crypto tax reporting went live. Sanctions enforcement changed after major court rulings.

If your last review predates all that, this guide is your reset on blockchain compliance and crypto compliance. I will cover what blockchain compliance requires in 2026. We will look at the US rules, the privacy trap everyone gets wrong, and how to build it right.

Key Takeaways

- Blockchain compliance means aligning your network, app, and transactions with the laws that apply.

- Blockchain compliance covers AML, KYC, sanctions, data privacy, tax reporting, and licensing requirements.

- In the US, the rulebook spans FinCEN, OFAC, the SEC and CFTC, the IRS, and state regulators like NYDFS.

- 2025 reset the field: the GENIUS Act, the Tornado Cash reversal, and live crypto tax reporting.

- GDPR’s right to erasure clashes with a blockchain’s permanent record. The fix is to keep personal data off-chain.

- Compliance is the price of institutional adoption. Build it in from day one.

What Is Blockchain Compliance?

Blockchain compliance means making blockchain networks, applications, and transactions follow the laws and regulations that apply to them.

In practice, blockchain regulatory compliance covers several duties. You meet AML and KYC rules and screen for sanctions. You honor data-privacy law, report for tax, and hold the right licenses.

Compliance also runs both ways. You meet outside rules. You can also use the blockchain itself as a compliance tool, because its record is auditable and tamper-resistant.

Key Areas of Blockchain Compliance

- KYC and identity verification

- AML and transaction monitoring

- Sanctions screening

- Data privacy and protection

- Tax reporting and licensing

It helps to be precise here, because the terms blur. A blockchain is a shared ledger. It records transactions in blocks linked by cryptographic hashes.

Cryptocurrency is one use of it. Web3 is a broader vision built on it. Compliance attaches to the activity you run, not to the word “blockchain” itself.

You May Also Like –

Why Blockchain Compliance Matters

Blockchain compliance and crypto compliance earn you market access. Banks will not hold your accounts without it. Payment processors will not touch your flows. Institutional customers will not sign.

It also builds trust, protects users from fraud, and reduces risk. And it keeps you clear of penalties that can reach the billions. Treat it as an on-ramp to legitimacy, not a brake on innovation.

The Core Tension: Decentralization vs. Regulation

Here is the structural challenge. Blockchains are decentralized, borderless, and pseudonymous. Most regulations were written for identifiable intermediaries in one country.

A transaction can cross a dozen borders in seconds. Several countries may all claim a say. Good design closes that gap on purpose. You decide who is accountable, where data lives, and how each duty is met.

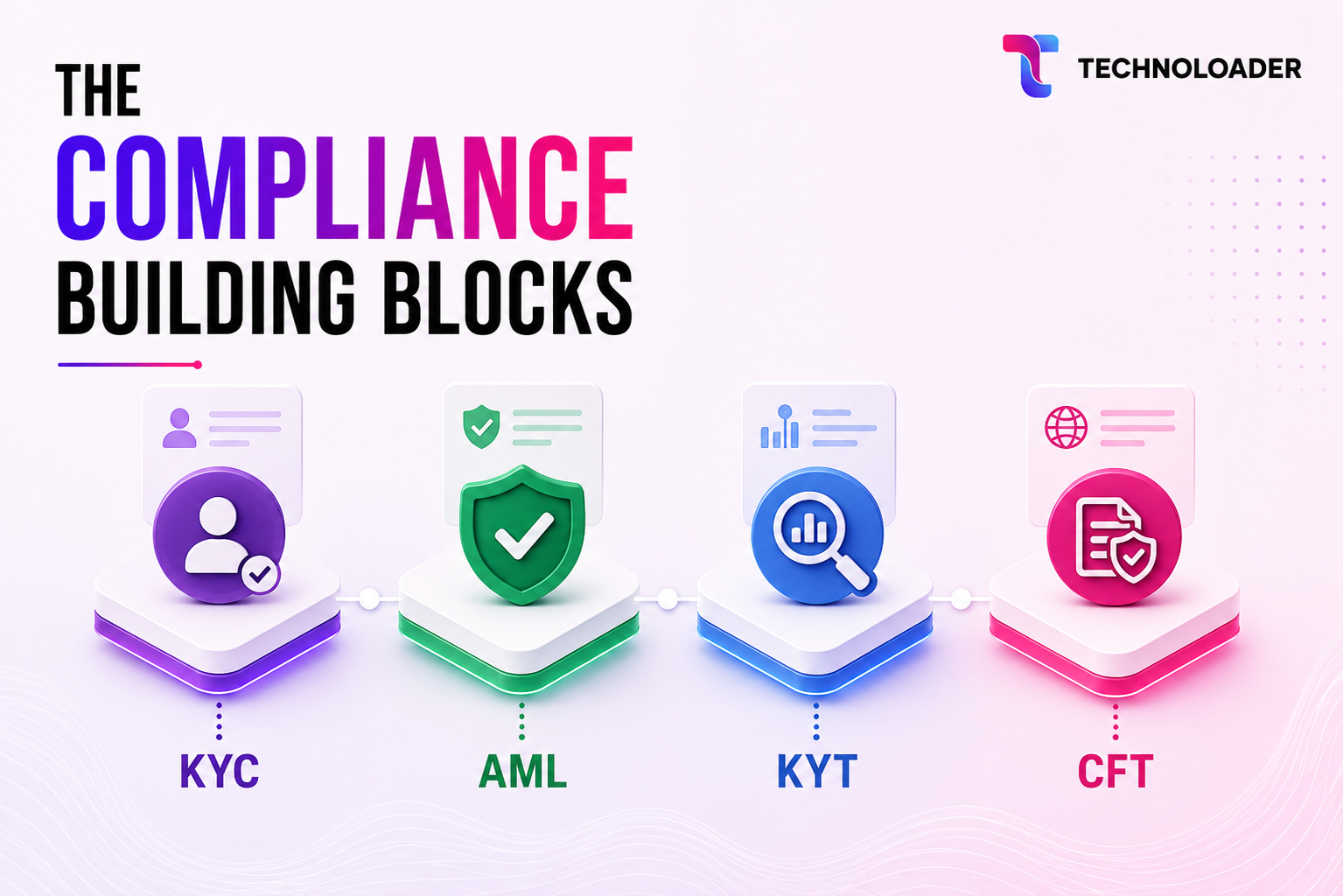

The Compliance Building Blocks: KYC, AML, KYT, and CFT

First, you need the vocabulary every regulated blockchain business uses. These four controls appear in almost every crypto compliance and blockchain regulatory framework worldwide.

KYC and KYB (Know Your Customer / Business)

KYC, or Know Your Customer, means verifying who your customer is before and during your relationship.

It starts with a Customer Identification Program. You collect and check identity documents. Then Customer Due Diligence assesses risk, with Enhanced Due Diligence for higher-risk cases. KYB applies the same checks to business customers and their owners.

AML and CFT (Anti-Money Laundering)

AML, or Anti-Money Laundering, is the set of controls that stop illicit funds from looking legitimate.

A real AML compliance program has several parts. It includes a written risk assessment, transaction monitoring, sanctions screening, recordkeeping, and reporting.

In the US, suspicious activity reports may be required for transactions above certain thresholds, while cash transactions above $10,000 can trigger reporting obligations.

CFT, Countering the Financing of Terrorism, is its partner. You will almost always see them paired as “AML/CFT.”

KYT (Know Your Transaction)

KYT, or Know Your Transaction, means monitoring transaction data, including on-chain activity, for risk.

This is where blockchain helps both sides at once. The public ledger is permanently visible. This visibility is one reason smart contracts can automate compliance checks. So analytics can trace flows, cluster addresses, and flag exposure to known-bad sources. Many of these controls are now automated through smart contracts and compliance tools. Traditional finance cannot match that.

In one line: KYC verifies the person. KYB verifies the business. AML/CFT govern the program. KYT watches the transactions. Get these four right, and the rest is detail.

US Blockchain Regulations You Must Know in 2026

There is no single “blockchain law” in the United States. Blockchain regulatory compliance is split across several agencies. Each governs a slice of what you do.

Here is the map of US crypto compliance. A lot has changed in the last eighteen months.

FinCEN and the Bank Secrecy Act (MSB, SAR, CTR)

The Financial Crimes Enforcement Network (FinCEN) is the front line. Guidance from 2013, reaffirmed in 2019, set the rule.

If you exchange or administer convertible virtual currency, you are a money transmitter. That makes you a Money Services Business (MSB) under the Bank Secrecy Act.

So you register with FinCEN and run an AML program. Registration uses FinCEN Form 107 and must generally be renewed every two years. You file a Suspicious Activity Report (SAR) for suspicious activity of $5,000 or more, usually within 30 days. You file a Currency Transaction Report (CTR) for cash over $10,000.

For firms working on blockchain in banking, these banking compliance duties sit on top of existing BSA obligations.

You May Also Like –

The FATF Travel Rule and FinCEN’s $3,000 Threshold

The “Travel Rule” requires that sender and recipient information accompany a transfer. It comes from Recommendation 16 of the Financial Action Task Force (FATF), the global standard-setter.

It applies to Virtual Asset Service Providers (VASPs). A VASP exchanges, transfers, or custodies virtual assets for customers. In the US, the recordkeeping threshold is $3,000.

A proposal would lower it to $250 for cross-border transfers. It is still pending. FATF revised Recommendation 16 in June 2025. As of 2025, about 85 jurisdictions had Travel Rule laws.

OFAC Sanctions and SDN Screening

The Office of Foreign Assets Control (OFAC) enforces US sanctions. It does so on a strict liability basis. You can be liable without intent.

OFAC lists specific crypto addresses on its Specially Designated Nationals (SDN) list. US persons must block dealings with them.

One nuance my team flags on every project: OFAC says its address listings are not exhaustive. So screening cannot rely on the SDN list alone. The maximum civil penalty rose to $377,700 per violation in January 2025.

Sanctions enforcement also saw its biggest reversal yet. In late 2024, a federal appeals court ruled that OFAC overstepped on Tornado Cash.

OFAC removed Tornado Cash from the SDN list on March 21, 2025. A court later barred it from re-sanctioning those immutable contracts. Criminal cases against individuals continued.

SEC, CFTC, and the GENIUS Act (Stablecoins)

The Securities and Exchange Commission (SEC) changed direction in 2025. It formed a Crypto Task Force in January.

It replaced the custody rule SAB 121 with SAB 122, effective January 30, 2025. It also dropped several flagship cases, including ones against major US exchanges.

The Commodity Futures Trading Commission (CFTC) still oversees crypto commodities and derivatives.

The headline change is legislative. The GENIUS Act became law on July 18, 2025. It is the first major US federal crypto statute.

It licenses payment-stablecoin issuers and requires 100% reserve backing with monthly disclosures. It puts issuers under the Bank Secrecy Act. Its core market restriction phases in about three years after signing.A broader market-structure bill, the CLARITY Act, passed the House.

IRS Form 1099-DA (Tax Reporting)

Tax reporting is no longer vague. The Internal Revenue Service (IRS) introduced Form 1099-DA for digital-asset brokers. It applies to transactions on or after January 1, 2025.

The first forms reach taxpayers in early 2026. Gross proceeds are reported for 2025. Cost-basis reporting phases in for transactions on or after January 1, 2026.

State Rules and the NYDFS BitLicense

Federal rules are only part of it. Most states also require a money-transmitter license. New York runs its own regime.

The New York State Department of Financial Services (NYDFS) BitLicense has a $5,000 application fee. It also asks for a large minimum net capital, often cited as around $500,000.

Approval often takes nine to twelve months. A limited-purpose trust charter is an alternative path.

The US rulebook in one paragraph: FinCEN governs AML and KYC. OFAC governs sanctions. The SEC and CFTC split asset classification. The IRS handles tax reporting. The states add licensing. If your activity touches money movement, assume more than one applies.

You May Also Like –

Blockchain vs. Data Privacy: GDPR and the Right to Be Forgotten

Most blockchain compliance content gets this topic wrong. I want to be precise.

Our scope here is the US. Still, the EU’s General Data Protection Regulation (GDPR) reaches across borders. It applies to any organization that processes the personal data of people in the EU.

So if you serve EU users, you are on the hook. The maximum fine is 20 million euros or 4% of global annual turnover, whichever is greater.

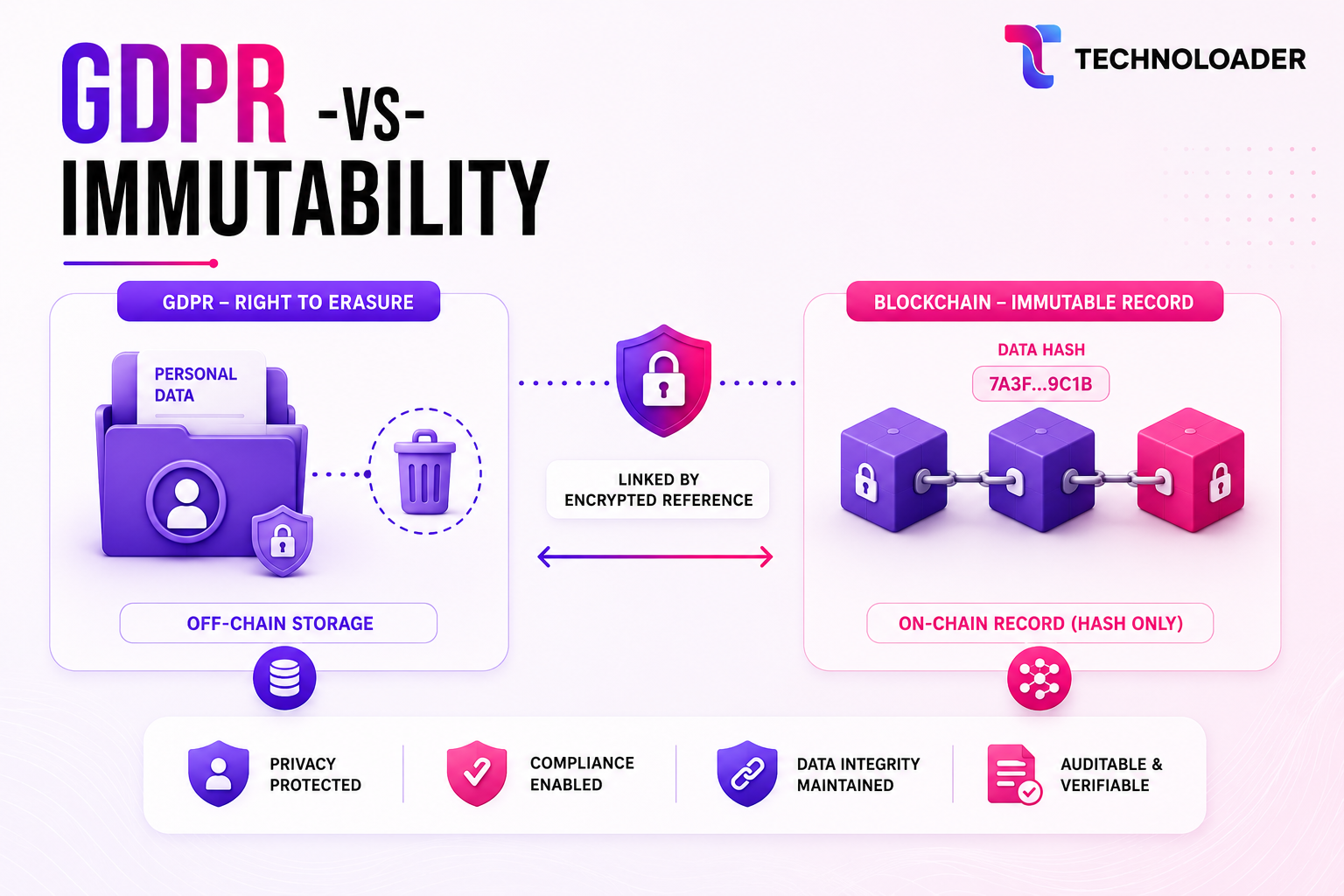

The Immutability vs. “Right to Erasure” Problem

GDPR’s Article 17 gives people the right to have their personal data erased. A blockchain is append-only and tamper-resistant. So data written on-chain generally cannot be altered or deleted.

European regulators accept that on-chain erasure “might be technically impossible.” That leads to one clear rule: do not put personal data on-chain in the first place. These legal challenges appear across regulated blockchain applications.

Is a Hash Still Personal Data? (Pseudonymization, Not Anonymization)

A common shortcut is to hash personal data and call it solved. It usually is not.

Under European guidance, hashing is pseudonymization, not anonymization. A hash, even a salted one, can still be personal data.

That holds if the original value can reasonably be re-derived or linked back. Data only leaves GDPR’s scope when re-identification is no longer reasonably possible.

How to Reconcile Blockchain With GDPR

The fix is an engineering pattern, not a slogan. Keep personal data off-chain in a controlled store. Anchor only a hash or pointer on-chain, so you can prove integrity without exposing the data.

Where you need ciphertext, use encryption plus key destruction. This is often called “crypto-shredding.” Destroying the keys is a recognized cryptographic-erase method, and it renders the data unintelligible.

Redactable or chameleon-hash blockchains exist, but they remain experimental. One honest caveat my engineers always state: destroying off-chain data or keys makes a record unreadable. It does not delete the on-chain entry.

Decision box: Should personal data ever go on-chain? No. Store personal data off-chain in a system you control. Write only a hash or pointer to the chain. This keeps integrity intact while you can still honor erasure requests.

GDPR for US Companies + the CCPA/CPRA Analog

For US companies, California’s CCPA, as amended by the CPRA, is the closest domestic equivalent. As of 2025, it generally applies under three thresholds.

Your gross annual revenue exceeds $26.625 million. You handle the data of 100,000 or more California residents. Or you draw at least half your revenue from selling or sharing personal information.

Administrative fines reach $2,663 per violation. They rise to $7,988 for intentional violations or those involving minors. The same off-chain design approach usually supports both GDPR and CCPA compliance.

You May Also Like –

How Blockchain Is Made Compliant: Tools and Techniques

Knowing the rules is half the job. The other half is engineering a system that meets them. This is where blockchain compliance becomes real design choices my team makes every week.

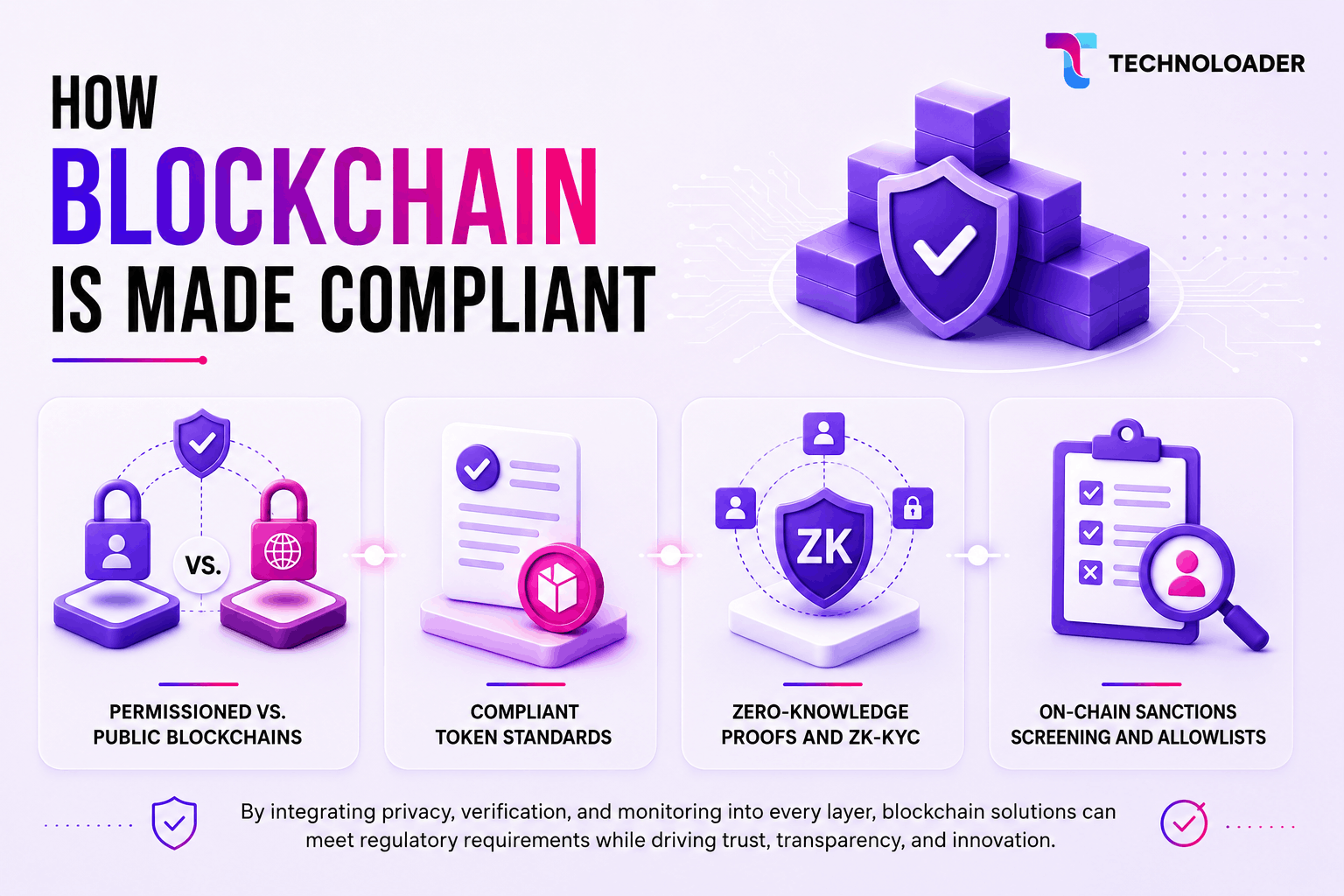

Permissioned vs. Public Blockchains

The first decision is the network type. A public chain is open to anyone and has no central controller. That makes accountability and data control harder.

A permissioned (private) network restricts who can join, validate, and read. You get an identifiable controller, access controls, and data governance.

For regulated data, permissioned designs make KYC and GDPR alignment much easier. They are never automatically compliant, though.

You May Also Like –

Compliant Token Standards (ERC-3643, ERC-1404)

Compliance rules can also be embedded in the token itself. ERC-3643, known as T-REX, is a permissioned, ERC-20-compatible standard for security tokens. Transfers only complete between verified, eligible wallets. It builds on-chain identity checks, freeze, and recovery.

ERC-1404 is a lighter restricted-transfer standard. It lets a token allow or deny a transfer and return a reason code. Both apply transfer restrictions at the smart contract level. But the tooling enforces only what you configure. Correct KYC and legal setup still sit behind it.

Zero-Knowledge Proofs and ZK-KYC

One promising technique is the zero-knowledge proof. It lets one party prove a statement is true without revealing the data behind it.

Applied to crypto compliance, “ZK-KYC” can prove a user is verified, over 18, or not sanctioned. It does so without exposing the personal details.

I will be candid about maturity. Zero-knowledge proofs are production-grade in some settings. But ZK-KYC for regulatory use is still emerging, not a settled standard.

On-Chain Sanctions Screening and Allowlists

Sanctions screening can run in two places. You can screen off-chain, before a transaction is signed. You can also screen on-chain through permissioned allowlists that only allow approved addresses to transact.

Remember the OFAC caveat from earlier. The SDN list is not exhaustive. So good screening combines list checks with risk analytics. It never treats the list as the whole job.

The compliance toolkit in one line: choose a permissioned design for regulated data. The private vs. public blockchain decision often determines compliance complexity. Enforce eligibility with compliant token standards. Prove facts with zero-knowledge where you can. And monitor risk continuously, not once.

The Cost of Non-Compliance: Penalties and Enforcement

The downside is not theoretical. In November 2023, Binance agreed to pay $4.3 billion to settle AML and sanctions violations. That included a $3.4 billion penalty to FinCEN, the largest in its history, plus about $968 million to OFAC.

Earlier enforcement actions established the pattern. BitMEX faced penalties of up to $100 million in 2021. Bittrex settled for about $29.3 million in 2022.

The scale of illicit activity keeps regulators focused. According to Chainalysis, illicit addresses received a record $154 billion in 2025. That is still under 1% of all crypto activity. Stablecoins now account for roughly 84% of that illicit volume.

The lesson I draw for clients is simple. Enforcement is real and expensive for businesses that ignore crypto compliance obligations. But it concentrates on businesses that ignored controls a sound program would have caught.

How to Build a Compliant Blockchain Solution

After 450+ projects, my team follows one sequence. It keeps compliance from becoming a launch-blocker. The process works for both crypto exchanges and enterprise blockchain projects.

- Map your obligations by activity, jurisdiction, and user base. Then you know which rules from Section 3 apply.

- Design data off-chain by default, anchoring only hashes on-chain. This approach makes privacy compliance easier by design.

- Choose the right network, leaning toward permissioned networks for regulated or personal data.

- Integrate the controls: KYC and KYB onboarding, AML monitoring, KYT analytics, Travel Rule messaging, and sanctions screening.

- Audit the code, because a compliant design still fails if the smart contracts are insecure.

- Keep counsel and monitoring ongoing, since rules and sanctions lists change constantly.

This is the work our blockchain development team does for regulated clients, from exchanges to tokenization platforms. Many organizations rely on external compliance specialists. We keep blockchain compliance, engineering, and delivery in-house.

You May Also Like –

Frequently Asked Questions

What is blockchain compliance?

Blockchain compliance means making a blockchain network, app, and its transactions follow the laws that apply to them. That covers AML and KYC rules, sanctions screening, data privacy, tax reporting, and licensing. It protects users, prevents penalties, and supports institutional adoption.

What is the legal compliance of blockchain in the US?

In the US, several regulators apply at once. FinCEN covers AML and KYC under the Bank Secrecy Act. OFAC covers sanctions. The SEC and CFTC handle asset classification. The IRS handles tax via Form 1099-DA. State agencies such as NYDFS handle licensing.

What are the key areas of blockchain compliance?

There are five core areas. The first is customer identity (KYC and KYB). The second is anti-money-laundering programs (AML and CFT). The third is transaction monitoring and sanctions screening (KYT). The fourth is data privacy (GDPR and CCPA). The fifth is tax reporting and licensing. Most frameworks combine these same blocks.

Is blockchain GDPR compliant?

It can be, if you design it correctly. On-chain data generally cannot be deleted. So you keep personal data off-chain and write only a hash on-chain. You also use encryption with key destruction where needed. Storing personal data on-chain is what creates the conflict.

What is the crypto Travel Rule?

The Travel Rule comes from FATF Recommendation 16. It requires sender and recipient information to travel with a virtual-asset transfer between regulated providers (VASPs). In the US, the recordkeeping threshold is $3,000.

What is the difference between KYC, AML, and KYT?

KYC verifies who a customer is. AML is the broader program that detects and prevents money laundering. KYT is ongoing monitoring of transactions, including on-chain activity, for suspicious patterns. They work together, not as substitutes.

Are blockchain transactions anonymous?

No. Most public blockchains are pseudonymous rather than anonymous. Every transaction tied to an address is permanently public. Analytics can cluster addresses and sometimes link them to real identities, especially at fiat on-ramps.

Do I need a license to run a blockchain or crypto business in the US?

Often, yes. Many crypto businesses must register with FinCEN as a money services business and hold state money-transmitter licenses. New York generally requires a NYDFS BitLicense. There is no single blockchain compliance certification that guarantees compliance. What matters is registering, licensing, and running the right controls. Confirm with counsel.

Conclusion

Blockchain compliance is what turns a blockchain project into a business that can scale. The US rulebook is becoming clearer, the privacy challenge is solvable, and the right compliance controls can be built directly into your product.

The rules are knowable. The privacy problem is solvable with the right architecture. And the tooling keeps improving.

The work is to design it from the start. Map your obligations. Keep personal data off-chain. Choose the right network. Build the controls into the product, not around it.

Do that, and compliance stops being a risk you fear. It becomes an advantage you own.

In my experience, the strongest blockchain products are not the ones that add compliance later. They are the ones who design it into the architecture from day one.

If you are planning a regulated blockchain product, talk to our blockchain engineers about building compliance into your architecture from day one.

Vipin Kumar

Vipin Kumar is the CEO of Technoloader, a leading blockchain development company. With deep expertise in emerging technologies, he drives innovation in Web3, gaming, and crypto solutions. He is passionate about delivering robust and scalable tech that transforms businesses in the digital age.

Published in Blockchain Development