+91 7014607737

+91 7014607737

info@technoloader.com

info@technoloader.com

Table of Contents

In business, trust is everything. But trust is also expensive.

Companies spend a huge amount of time and money on audits, verifications, intermediaries, and compliance systems just to ensure that records are correct and transactions are secure.

That’s where blockchain comes in!

Blockchain technology helps businesses create a system in which data is secure, transparent, and nearly impossible to manipulate, while also reducing reliance on third parties.

In fact, a report from Markets and Markets estimates that the global blockchain market was USD 32.99 billion in 2025 and will grow to USD 393.45 billion by 2030. This shows how quickly businesses are adopting blockchain solutions.

Want to know how blockchain will benefit your business? Well, that’s what this blog is for!

Have a look!

What is Blockchain?

A blockchain is basically a distributed database or ledger shared across the nodes of a computer network. It is known for its role in cryptocurrency systems as it helps in maintaining a secure and decentralized record of transactions. But blockchain is not limited to cryptocurrency uses. It can be used to make data in any industry immutable, which means the data can’t be altered.

The easiest way to understand blockchain is to think of it like a shared online record book that multiple parties can access. Every time a new transaction or record is added, it is saved as a “block.” These blocks are then linked together in a sequence, which forms a “chain” – that’s why it’s called blockchain.

Once information is added to the blockchain, it becomes permanent and verifiable, allowing everyone in the network to trust the data without a third-party intermediary such as a bank, auditor, or central authority.

Traditional Systems vs. Blockchain Technology

To understand why blockchain is considered a game-changer, it is important to compare it with traditional systems. Here we go!

| Feature | Traditional Systems | Blockchain Technology |

|---|---|---|

| Data Storage | Stored in a central database/server | Stored across a distributed network |

| Control | Controlled by one organization | Shared control across the network participants |

| Trust Model | Requires third parties (banks, auditors, intermediaries) | Trust is built into the system using cryptography |

| Transparency | Limited visibility, depends on permission from the owner | High transparency (shared ledger for authorized users) |

| Security | Higher risk if the central server is hacked | Strong security due to decentralization + encryption |

| Data Changeability | Records can be modified or deleted | Records are tamper-resistant and nearly immutable |

| Transaction Speed | Often slower due to verification layers | Faster in many cases due to peer-to-peer validation |

| Cost | Higher due to intermediaries and manual processes | Can reduce costs by minimizing intermediaries |

| Audit & Tracking | Audits require manual verification and logs | Easier audits due to traceable transaction history |

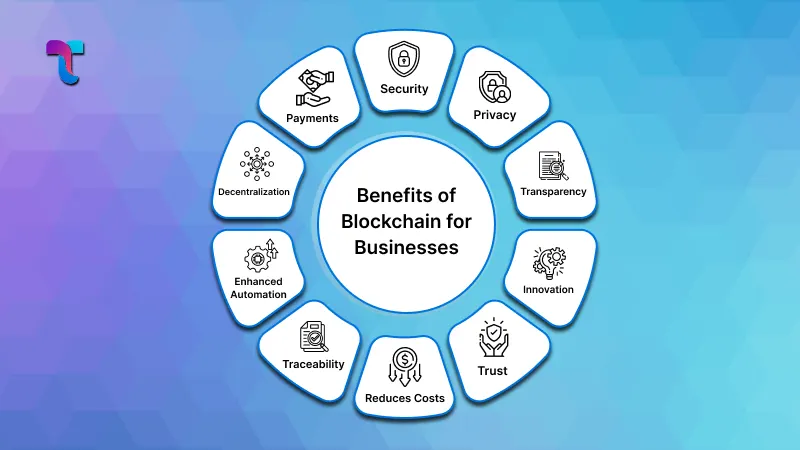

Strategic Benefits of Blockchain for Businesses

With its wide range of applications, many businesses are now using blockchain to improve processes and even create new business models. Here are some more benefits of blockchain that every business should consider:

Security

Security plays an important role for any business, especially those dealing with transactions.

In blockchain, security is high, and it stems from how the system works. Each piece of data or transaction, known as a block, is stored chronologically using a cryptographic mechanism. After a block has been added to the chain, it is nearly impossible to go back and change or remove any data.

Another key reason blockchain is trusted is that transactions are validated through network consensus. This means the transaction is approved only when multiple participants in the network agree. After confirmation, the data becomes immutable, meaning it cannot be edited, deleted, or manipulated.

Learn more about: how to secure a blockchain app from attacks

Privacy

In today’s digital world, data is one of the most valuable assets for businesses. Protecting sensitive information is becoming harder because traditional systems often store data in centralized databases that can be misused.

Blockchain improves privacy by giving users and businesses more control over their data. Instead of sharing complete information with every party, blockchain systems can be designed so that only the required details are visible, while the rest remains protected.

Even in cryptocurrency networks where transactions are traceable, user identity is not always directly linked to the transaction. This creates a privacy advantage for businesses.

Transparency

Transparency is one of the main benefits of blockchain for businesses, especially when multiple parties are involved. Since blockchain works as a shared ledger, all participants can view the same transaction history in real time.

Unlike traditional systems, where each business maintains its own database and records can differ across departments, blockchain ensures that all participants use a single, consistent version.

Every transaction becomes a permanent part of the ledger, which makes tracking and verification much easier. This level of transparency can be helpful for government services, audits, and even electronic voting.

Innovation

Many businesses are exploring blockchain to solve complex operational challenges and replace outdated centralized systems.

For example, blockchain in healthcare can help securely store medical records. Once a record is created and verified, it can be written to the blockchain, which ensures it cannot be edited or tampered with.

Blockchain can also support businesses in recruitment and verification. For instance, verified certificates and records can be stored on the blockchain, which makes it easier for recruiters to verify credentials and reduce fraudulent claims in resumes. This saves time and improves trust in hiring processes.

Trust

Trust is a major factor in businesses. And blockchain strengthens trust by ensuring that records and transactions are transparent, traceable, and difficult to manipulate.

Because blockchain data is verified by the network and stored permanently, customers feel more confident that transactions are genuine, records are accurate, and the system can’t be controlled by one party.

For businesses, this trust leads to stronger customer relationships, improved brand credibility, and higher long-term loyalty. When customers know a company uses blockchain for secure payments, it automatically boosts confidence in that brand.

Reduces Costs

Blockchain can reduce business costs by minimizing manual work and eliminating intermediaries.

In traditional systems, businesses often pay banks, payment processors, and third-party service providers for transaction verification and recordkeeping. Blockchain reduces these expenses because transactions can be validated directly through the blockchain network.

It also reduces operational costs by improving auditing and reporting. Since blockchain records are already time-stamped, structured, and verifiable, businesses spend less time on paperwork, repetitive data entry, and long audit processes.

Traceability

Traceability means being able to track a transaction. This is extremely important for industries such as manufacturing, logistics, food supply, pharmaceuticals, and retail.

Blockchain improves traceability by recording every step in the supply chain on a shared ledger. Every time a product moves – from manufacturer to distributor, from distributor to warehouse, from warehouse to customer – the event can be logged securely.

This makes it easier to verify authenticity, detect supply chain issues early, identify where delays or quality problems started, and build customer trust through verified product history.

Enhanced Automation

Blockchain supports automation through smart contracts. These are basically self-executing digital agreements stored on the blockchain that automatically perform actions when predefined conditions are met.

For example, payments are released automatically upon delivery confirmation, commissions are distributed instantly according to business rules, and agreements between parties are executed without manual approvals.

This reduces delays, human errors, and dependency on middlemen. For businesses, smart contract automation improves speed, accuracy, and operational efficiency.

Before deploying smart contracts at scale, enterprises usually validate workflows, performance, and security through a blockchain proof of concept for enterprises.

Planning to automate workflows using smart contracts?

Decentralization

Traditional systems are centralized, meaning a single organization or server controls the entire database. This creates risks such as a single point of failure, increased susceptibility to manipulation, and dependence on a single authority.

Blockchain introduces decentralization, in which records are shared across a network rather than controlled by a single entity. This makes systems more reliable and resistant to fraud.

Decentralization also improves trust in business operations because no single party can secretly change records. For businesses, it creates stronger accountability and increases customer confidence.

Payments

Blockchain is widely recognized for enabling secure and efficient digital payments. Its decentralized ledger makes transaction recording more reliable, transparent, and traceable.

Blockchain-based payments allow businesses to send and receive money without relying entirely on traditional banking networks. This can be especially beneficial for cross-border payments, faster settlement times, reducing intermediary charges, and improving cash flow.

Many well-known companies have already explored crypto and blockchain payment solutions to make payments smoother, faster, and more secure.

Blockchain Use Cases Across Industries

Blockchain is often associated only with cryptocurrency, but in reality, its value lies in how it manages data and trust. it records information in a way that is transparent, traceable, and extremely difficult to change.

That’s why many industries are using blockchain to solve real business problems, such as fraud, inefficiency, lack of transparency, and heavy reliance on middlemen.

Below are the most common real-world blockchain use cases across industries:

Finance & Banking

Banks and financial institutions use blockchain to improve payment systems, especially for cross-border transactions. Traditional international payments can take 1 to 3 days and involve multiple intermediaries. Blockchain in banking makes transfers faster, more trackable, and often lower cost.

For example, JPMorgan launched blockchain-based solutions under its Onyx division to support instant settlement and modernize institutional transactions.

Supply Chain & Logistics

Supply chains involve many parties, like manufacturers, warehouses, transport companies, retailers, and more. Blockchain helps supply chains track products from origin to delivery, ensuring the data cannot be altered later. This improves traceability, reduces fraud, and makes recalls easier.

For example, Walmart used blockchain via IBM Food Trust to improve the traceability of food products like leafy greens. It helps in identifying sources quickly during food safety checks.

Healthcare

Healthcare requires the storage and sharing of sensitive medical data. Blockchain in healthcare enables secure record storage and controlled access, where only authorized people can view or update data. It improves privacy and reduces the risk of tampering.

For example, Estonia used blockchain technology to help secure government systems, including healthcare records, which ensures the integrity of digital medical data.

Government & Public Records

Governments handle important public records such as land registry, identity documents, licenses, and certificates. Blockchain can help create tamper-proof records, increase transparency, and reduce corruption.

For example, Georgia implemented blockchain technology for land registration to improve trust, prevent record manipulation, and enable faster verification of property documents.

Real Estate

Property purchases involve heavy paperwork and lengthy verification. Blockchain in real estate can store land/property records securely and improve transparency in ownership transfers. It can also help automate agreements through smart contracts.

For example, Dubai has explored blockchain initiatives for property documentation and modernizing real estate processes.

Education & Hiring

Fake degrees and fake certificates are common in hiring. Blockchain helps store verified credentials such as degrees and skill certificates, so employers can check authenticity instantly, and without manual verification.

For example, MIT issued blockchain-based digital diplomas that can be verified online. This helps reduce fraud and simplifies credential validation.

Media & Entertainment

Content ownership and royalty payments are major problems in the media. Blockchain can help creators prove ownership, track how content is used, and distribute royalties in a transparent way.

For example, Audius uses blockchain to support music distribution with a creator-first approach.

Permissioned, Private & Hybrid Blockchains in 2026

When most people hear the word blockchain, they immediately think of public networks like Bitcoin and Ethereum. But in the business world, most companies are not using fully public blockchains for day-to-day operations.

Instead, enterprises prefer blockchain models that offer privacy, controlled access, faster performance, and compliance support. That’s where permissioned, private, and hybrid blockchains come in.

Let’s understand each of them now!

Permissioned Blockchain

A permissioned blockchain is one in which only approved participants can join the network, view the ledger, or validate transactions. This is ideal for business networks because companies don’t want unknown parties to access internal transaction data.

In a permissioned blockchain:

- The network is controlled by an organization or consortium

- Participants are verified (e.g., banks, suppliers, partners)

- Transactions are still transparent inside the network

Private Blockchain

A private blockchain is a blockchain owned and controlled by a single organization. It is typically used inside a company for internal operations. Unlike permissioned blockchains, where multiple organizations may participate, private blockchains are mostly used for:

- Internal audits

- Secure record keeping

- Enterprise automation

- Departmental data sharing

Hybrid Blockchain

A hybrid blockchain combines features of both public and private blockchains. It lets companies keep sensitive data private while still using public blockchain features when required.

In a hybrid blockchain:

- Confidential business data stays private (accessible only to approved users)

- Selected information can be made public for transparency (like proofs, verification records, timestamps)

Not sure which blockchain model suits your business?

Challenges of Blockchain & How Enterprises Overcome Them

Blockchain adoption is increasing across industries. With that comes a wide range of challenges. Let’s discuss them one by one!

Integration with Existing Systems

One of the biggest challenges enterprises face is integration. Most businesses already run on mature systems like ERP platforms, CRMs, and more. These systems are deeply connected to daily operations. Blockchain cannot simply replace them because it is not designed to function as an “all-in-one” software.

To overcome this, enterprises implement blockchain as an additional layer of trust. The standard approach is to connect blockchain via APIs and middleware, so the existing system continues to work, usually while blockchain records critical events such as approvals, transfers, or certifications.

Scalability and Performance Limitations

Enterprises handle high volumes of operations daily. However, many blockchain networks can face limitations in transaction speed, costs, and throughput. If a company needs to record large numbers of transactions every minute, performance can become a barrier.

Enterprises solve this by choosing the right blockchain ecosystem protocol. In 2026, many businesses are adopting permissioned or private blockchains that offer greater control and higher performance than public networks.

Privacy & Confidential Business Data

Privacy is another major concern because blockchain is naturally designed for transparency. But businesses cannot expose sensitive information such as customer details, financial transactions, employee records, pricing models, or supplier contracts.

To address this challenge, enterprises implement blockchain systems that control data visibility. This is why private, permissioned, and hybrid blockchains are becoming the enterprise standard.

Legal & Regulatory Compliance

Blockchain brings strong auditability, but it also raises regulatory questions. Enterprises must comply with strict laws on data retention, KYC/AML/GDPR, consumer protection, and privacy policies.

Enterprises overcome this by designing blockchain implementations that are legally compatible. In practice, many businesses avoid storing personal information directly on-chain. Instead, they store encrypted proofs, transaction IDs, or references to ensure compliance requirements are met.

Lack of Skilled Talent & Technical Complexity

Blockchain development requires specialized expertise, and enterprises often struggle to find skilled developers who understand smart contracts, cryptography, security design, blockchain infrastructure, and governance.

To handle this, enterprises usually adopt one of two approaches. Either they partner with blockchain development firms and consultants, or they upskill their internal engineering teams through training and controlled pilot projects.

The End Note

That’s it for this blog!

Blockchain is now helping businesses improve security, transparency, trust, and efficiency in real-world operations. Whether it’s tracking products in the supply chain, securing sensitive records, automating agreements, or reducing fraud, blockchain is clearly proving its value across industries.

At the same time, it’s important to be practical. Blockchain adoption isn’t about jumping on a trend — it’s about choosing the right use case, selecting the right type of blockchain, and building a system that actually solves a business problem.

So if you are a business owner or decision-maker looking to future-proof your operations, blockchain is worth considering.

And if you are planning to explore blockchain for your business and want the right guidance, we, at Technoloader, can help you build secure, scalable, and business-ready blockchain solutions tailored to your industry needs.

Get in touch with us now!

Frequently Asked Questions

What is blockchain in simple words?

Blockchain is a distributed ledger system that stores information in a secure, tamper-resistant way. Instead of storing data in a single central database, blockchain distributes it across a network, making records transparent, traceable, and tamper-resistant.

How does blockchain benefit businesses?

Blockchain helps businesses improve security, transparency, traceability, and trust. It can also reduce operational costs by removing intermediaries and automating processes using smart contracts.

Is blockchain only used for cryptocurrency?

No, not at all! Cryptocurrency is just one use case of blockchain. Many industries use blockchain technology for supply chain tracking, digital identity verification, healthcare records, document authenticity, and fraud prevention.

Which industries benefit the most from blockchain?

Blockchain is widely used in:

- Finance & banking

- Supply chain & logistics

- Healthcare

- Government records

- Real estate

Is blockchain 100% secure?

No system is 100% secure, but blockchain is considered highly secure due to its cryptographic mechanisms and network-based validation. However, security also depends on the quality of smart contracts, network configuration, and system implementation.

What is the difference between public and private blockchains?

- Public blockchain: Open network, anyone can participate

- Private blockchain: Controlled by one organization; access is restricted

How does blockchain reduce costs for businesses?

Blockchain helps reduce costs by:

- Removing intermediaries

- Reducing manual paperwork and reconciliation

- Improving audit readiness

- Automating processes using smart contracts

What are smart contracts, and how do they help businesses?

Smart contracts are self-executing programs stored on a blockchain. They automatically perform actions when conditions are met, such as releasing payments after delivery confirmation. This reduces delays, errors, and manual effort.

Can blockchain help prevent fraud?

Yes, of course! Since blockchain records cannot be easily altered after confirmation, it becomes difficult to manipulate transactions. This is helpful for preventing fraud across areas such as supply chain, payments, identity systems, and document verification.

Is blockchain legal in India?

Yes, blockchain technology is legal in India. It is widely used in enterprise applications. However, crypto regulations may vary, so businesses should treat blockchain adoption and crypto-related services as different areas from a compliance perspective.

Deepa Manwani

Deepa Manwani is a Technical Content Writer at Technoloader with over 7 years of experience creating high-quality content across Blockchain, Web3, AI, and fintech. She specializes in translating complex technical concepts into clear, engaging, and informative content that helps businesses, developers, and users better understand emerging technologies. Her expertise includes writing technical blogs, technical documentation, whitepapers, platform guides, and in-depth content for crypto exchanges, DeFi platforms, trading systems, and enterprise software solutions. At Technoloader, she contributes to developing strategic content that supports product growth, strengthens brand credibility, and educates users about next-generation technologies shaping the future.

Published in Blockchain Development